All human beings have traits that make them unique: their fingerprints, eye color, car loan rates, etc.

Yes, you heard that right. While it’s true that your car loan rate isn’t exactly a trait, per se, it is one more thing that differentiates you from others. Why? Because most loans are customized to the borrower, which means you likely can’t predict the rate you’ll get just by polling your neighbors.

Still, a little research never hurts. Here’s the latest data on auto loans—and more importantly, how you can improve your odds of securing a good car loan rate yourself.

What Is a Good Car Loan Rate, Anyway?

Before we jump in, we should note that the term “good” is subjective. If you asked us about good ice cream flavors, we’d tell you the kinds that most people prefer (and we might even throw in our personal favorite), but we couldn’t definitively state that Cookies and Cream is good.

The same is true with vehicles. So instead of showing you good car loan rates and bad ones, we’ve gathered data on average rates. That way, you can enter the world of auto refinancing with a little more background knowledge than before — and decide what the term “good” means to you.

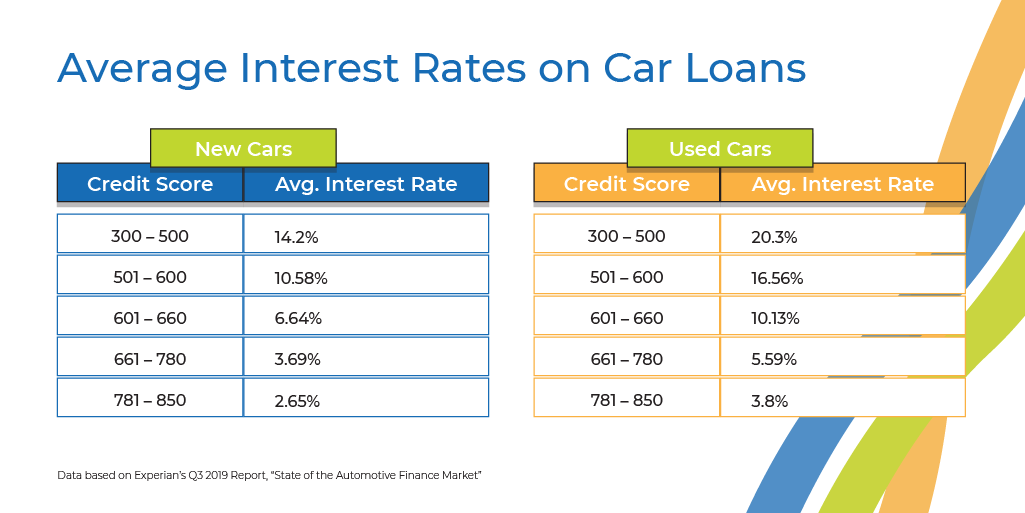

Experian, one of the US’s three major credit bureaus, recently released its findings on auto finance trends. The data (illustrated in the tables above) shows that interest rates vary widely depending on the borrower’s credit score.

On average, people with higher credit scores were offered lower interest rates. In fact, people with lower credit scores (600 and below) often had interest rates in the double digits, while people with credit scores of 700 and above could usually depend on an interest rate of around 5 percent.

(Recommended Reading: “How Does Car Loan Interest Work?”)

Factors that Can Affect Your Car Loan Rate

Don’t get us wrong; your credit score isn’t the only indicator of your auto loan rates. Lenders look at a number of things to determine their offer, including the following:

- Debt-to-income ratio

- Size of down payment

- Length of loan

- Age of vehicle

- Credit score

Each of these acts as a puzzle piece, helping your lender cobble together a big picture of your auto finances.

If that big picture isn’t exactly working in your favor, you still have options. By taking some time to increase your credit score, you may be able to qualify for a good car loan rate—or even refinance your auto loan down the road.

How to Improve Your Credit Score for a Good Car Loan Rate (and a Ton of Other Benefits!)

High credit scores are like the golden ticket of adulting. Having one can help you find better car insurance rates, get approved for more rental homes, qualify for higher credit card limits—and let’s be honest, the bragging rights aren’t half bad, either.

Fortunately, a good credit score isn’t nearly as elusive as one of Willy Wonka’s golden tickets. Focus on these five areas to get a fighting chance of improving your credit over time.

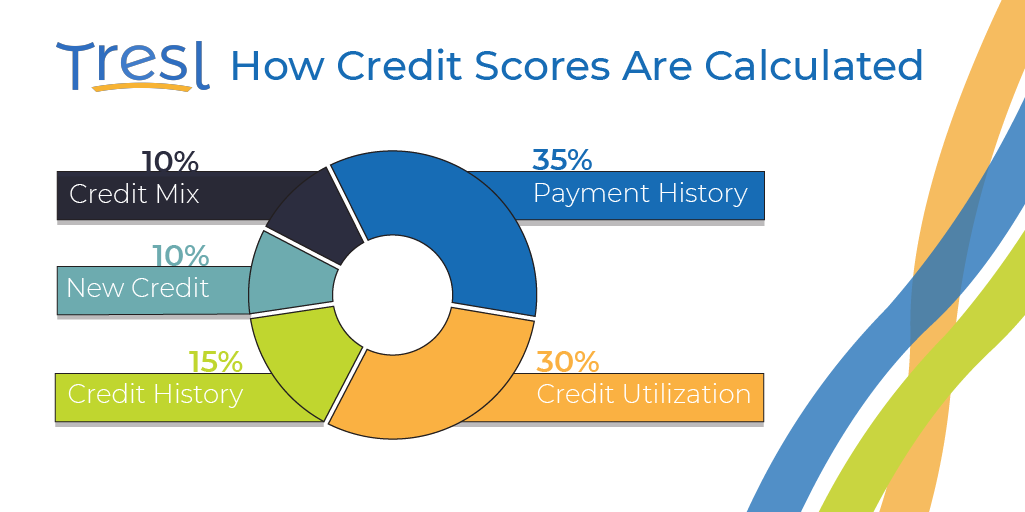

Note: In this article, we refer only to the FICO credit score. Other credit reporting systems, such as the VantageScore, may use different percentages and categories to calculate their scores.

Payment History

Let’s face it: People are less likely to trust you with their money if you have a history of forgetting to pay them back. It’s true for the $10 you borrowed from your friend for pizza last week, and it’s true for the $10,000 you’re asking from the bank.

That’s why lenders put such a big emphasis on your payment history. They want to know exactly how many payments you’ve missed so they can hedge their bets. (Don’t worry, it’s not personal. Experian’s stats show that auto delinquencies—aka past-due accounts—increased by 12% in the last three months of 2020.)

If your payment history is less than ideal, it may be bringing down your credit score—and your chances of finding a good car loan rate.

To prevent your credit score from dipping lower in the future, it’s important to pay any late bills, especially if they’ve already gone to collections. Payments that are late by 30 days or more will typically stay on your credit score for seven years, so it’s vital that you avoid any additional late payments.

Credit Utilization

Of course, payment history is only one slice of the pie. (A little more than a third, to be exact.) Credit utilization makes up 30 percent of your credit score, which is only 5 percent less than your payment history.

Credit utilization refers to how much of your credit you use at once. Say you have a credit card with a $1,000 max, for example. If you spend $500 before paying it off, you’ve utilized 50 percent of your credit.

Why does this matter? Generally speaking, lenders tend to trust people who use less of their credit because it shows that the borrower doesn’t rely too heavily on it.

Here’s a good rule of thumb: Aim to keep your credit utilization below 30 percent.

Credit History

If you’re new to borrowing, you probably don’t have very much data on your credit report. That means more risk for lenders. Still, everyone has to start somewhere, which is why most credit scoring models use it to determine about 15 percent of your credit score.

A lack of credit history may give you trouble when you’re looking for a good car loan rate. Lenders may ask you to have a co-signer (or co-borrower) who will vouch for your ability to pay back your loan. Later on, you may be able to remove a co-signer from the car loan through auto refinancing.

New Credit

New credits may sound similar to credit history, but it actually refers to an entirely different category. The New Credit section of your credit report shows the number of new accounts you’ve recently opened and the number of hard inquiries you’ve made.

FICO only attributes 10 percent of your score to this data, so it often won’t affect your score as noticeably as, say, your payment history. That being said, every percentage point counts when you’re trying to get a better car loan rate.

A hard inquiry occurs when a lender needs to see a detailed version of your credit report. If, for instance, you apply for a mortgage, a hard inquiry will likely show up on your credit report. Then, perhaps three weeks later, you apply for a different mortgage. The second lender will see the first hard inquiry, which proves that you’ve applied for credit recently.

Credit Mix

Lenders want to see how you handle different types of credit, like mortgages, credit cards, car loans, etc. According to the FICO model, this accounts for 10 percent of your credit score, so it’s equally as important as the state of your new credit—which is to say tied for last.

To improve your credit mix, many experts suggest keeping old credit card accounts open. Though you may not use the account anymore, your credit mix will benefit from its existence.

A Good Car Loan Rate Is What You Make It

What is a good car loan rate? The answer is up to you.

By studying recent data and learning about the inner workings of credit scoring models like FICO, you might be able to better understand how your car loan rates rank next to people in similar demographics.

Ultimately, though, your rates are unique to your situation. Use this information as a guidepost for your auto finance decisions rather than a hard-and-fast rulebook.

Feel like you need a little more guidance? Contact us today to get access to a dedicated Tresl finance advisor.